- Normal Balances

When looking at a T-account for each of the account classifications in the general ledger, here is the debit or credit balance you would normally find in the account:

- Revenues and Gains Are Usually Credited

Revenues and gains are recorded in accounts such as Sales, Service Revenues, Interest Revenues (or Interest Income), andGain on Sale of Assets. These accounts normally have credit balances that are increased with a credit entry.

The exceptions to this rule are the accounts Sales Returns, Sales Allowances, and Sales Discounts—these accounts have debit balances because they are reductions to sales. Accounts with balances that are the opposite of the normal balance are called contra accounts; hence contra revenue accounts will have debit balances.

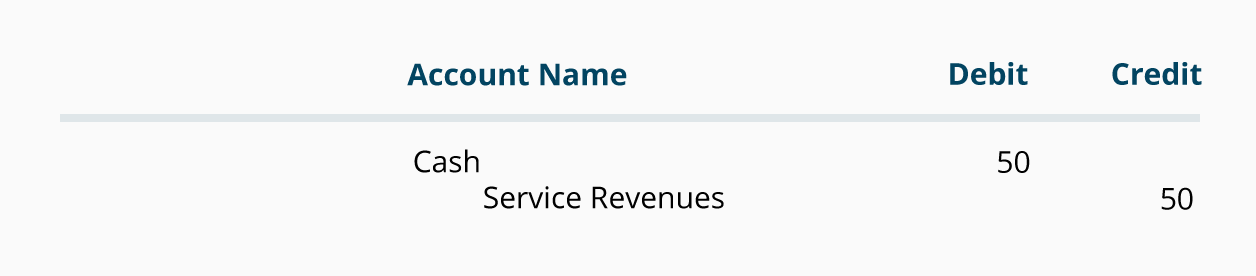

Let's illustrate revenue accounts by assuming your company performed a service and was immediately paid the full amount of $50 for the service. The debits and credits are presented in the following general journal format:

Whenever cash is received, the asset account Cash is debited and another account will need to be credited. Since the service was performed at the same time as the cash was received, the revenue account Service Revenues is credited, thus increasing its account balance.

Let's illustrate how revenues are recorded when a company performs a service on credit (i.e., the company allows the client to pay for the service at a later date, such as 30 days from the date of the invoice). At the time the service is performed the revenues are considered to have been earned and they are recorded in the revenue account Service Revenues with a credit. The other account involved, however, cannot be the asset Cash since cash was not received. The account to be debited is the asset account Accounts Receivable. Assuming the amount of the service performed is 400, the entry in general journal form is:

Accounts Receivable is an asset account and is increased with a debit; Service Revenues is increased with a credit.

- Expenses and Losses are Usually Debited

Expenses normally have their account balances on the debit side (left side). A debit increases the balance in an expense account; a credit decreases the balance. Since expenses are usually increasing, think "debit" when expenses are incurred. (We credit expenses only to reduce them, adjust them, or to close the expense accounts.) Examples of expense accounts includeSalaries Expense, Wages Expense, Rent Expense, Supplies Expense, and Interest Expense.

To illustrate an expense let's assume that on June 1 your company paid 800 to the landlord for the June rent. The debits and credits are shown in the following journal entry:

Since cash was paid out, the asset account Cash is credited and another account needs to be debited. Because the rent payment will be used up in the current period (the month of June) it is considered to be an expense, and Rent Expense is debited. If the payment was made on June 1 for a future month (for example, July) the debit would go to the asset account Prepaid Rent.

As a second example of an expense, let's assume that your hourly paid employees work the last week in the year but will not be paid until the first week of the next year. At the end of the year, the company makes an entry to record the amount the employees earned but have not been paid. Assuming the employees earned 1,900 during the last week of the year, the entry in general journal form is:

As noted above, expenses are almost always debited, so we debit Wages Expense, increasing its account balance. Since your company did not yet pay its employees, the Cash account is not credited, instead, the credit is recorded in the liability account Wages Payable. A credit to a liability account increases its credit balance.

To help you get more comfortable with debits and credits in accounting and bookkeeping, memorize the following tip:

Here's a Tip

To increase an expense account, debit the account.

- Permanent and Temporary Accounts

Asset, liability, and most owner/stockholder equity accounts are referred to as "permanent accounts" (or "real accounts"). Permanent accounts are not closed at the end of the accounting year; their balances are automatically carried forward to the next accounting year.

"Temporary accounts" (or "nominal accounts") include all of the revenue accounts, expense accounts, the owner drawing account, and the income summary account. Generally speaking, the balances in temporary accounts increase throughout the accounting year and are "zeroed out" and closed at the end of the accounting year.

Balances in the revenue and expense accounts are zeroed out by closing/transferring/clearing their balances to theIncome Summary account. The net amount in Income Summary is then closed/transferred/cleared to an owner equity account, such as Mary Smith, Capital (or to Retained Earnings if the company is a corporation). The owner drawing account (such asMary Smith, Drawing) is a temporary account and it is closed directly to the owner capital account (such as Mary Smith, Capital) without going through an income summary account.

Because the balances in the temporary accounts are transferred out of their respective accounts at the end of the accounting year, each temporary account will have a zero balance when the next accounting year begins. This means that the new accounting year starts with no revenue amounts, no expense amounts, and no amount in the drawing account.

By using many revenue accounts and a huge number of expense accounts, a company is certain to have easy access to detailed information on revenues and expenses throughout the year. This allows the management of the company to monitor the performance of all parts of the company. Once the accounting year has ended, the need to know the balances in these temporary accounts has also ended, so the accounts are closed out and reopened for the next accounting year with zero balances.

as a visual aid for seeing the effect of the debit and credit on the two (or more) accounts. (Learn more about accountants and bookkeepers in our

as a visual aid for seeing the effect of the debit and credit on the two (or more) accounts. (Learn more about accountants and bookkeepers in our